Home

Home

Artists

Artists

Search

Search

Recent

Recent

Random

Random

Posts

Posts

DMs

DMs

Tags

Tags

Random

Random

Importer

Importer

Import

Import

FAQ

FAQ

Account

Account

Register

Register

Favorites

Favorites

Login

Login

The Low Bollinger Band HO Algorithm – ‘Buy the Dip’ (Patreon)

Downloads

Content

Hi there and welcome to this post where I discuss the ‘Low_BBHO’ algorithm.

You can find this strategy file on github in multiple repositories (you have to be logged in btw.: https://github.com/search?q=Low_BBHO&type=code).

The strategy

This Low_BBHO strategy (created by the author Thorsten) is a example of an algorithmic approach designed around a "buy the dip" philosophy, using Bollinger Bands to identify attractive entry points. It combines Bollinger Bands and a flexible ROI configuration with defined stop-loss settings to enhance the potential for profit and minimize risk.

The strategy is configured to run on a rapid 1-minute timeframe, designed for high-frequency trades. But in this test my lowest timeframe is the 5 minute TF. The choice of this superlow 1 minute timeframe is probably aimed to capture short, potentially profitable movements in price over brief periods.

In terms of return on investment (ROI), the strategy has a detailed configuration that gradually lowers the target ROI over time. It has a initial ROI target of 8.5% as soon as the position is opened and reached. As time progresses, these targets reduce, with smaller ROI thresholds set at 7 minutes (1.1%), 19 minutes (0.7%), and selling out at 40 minutes.

The stop-loss parameter is also well-defined at -26.3%, a large margin that allows the strategy to endure some market fluctuations. However, this limit still acts as a protection mechanism against drastic losses.

The strategy does not employ a trailing stop loss, which means once a trade is in profit, there is no mechanism to progressively lock in gains as the price increases (and also possible skewed backtest results).

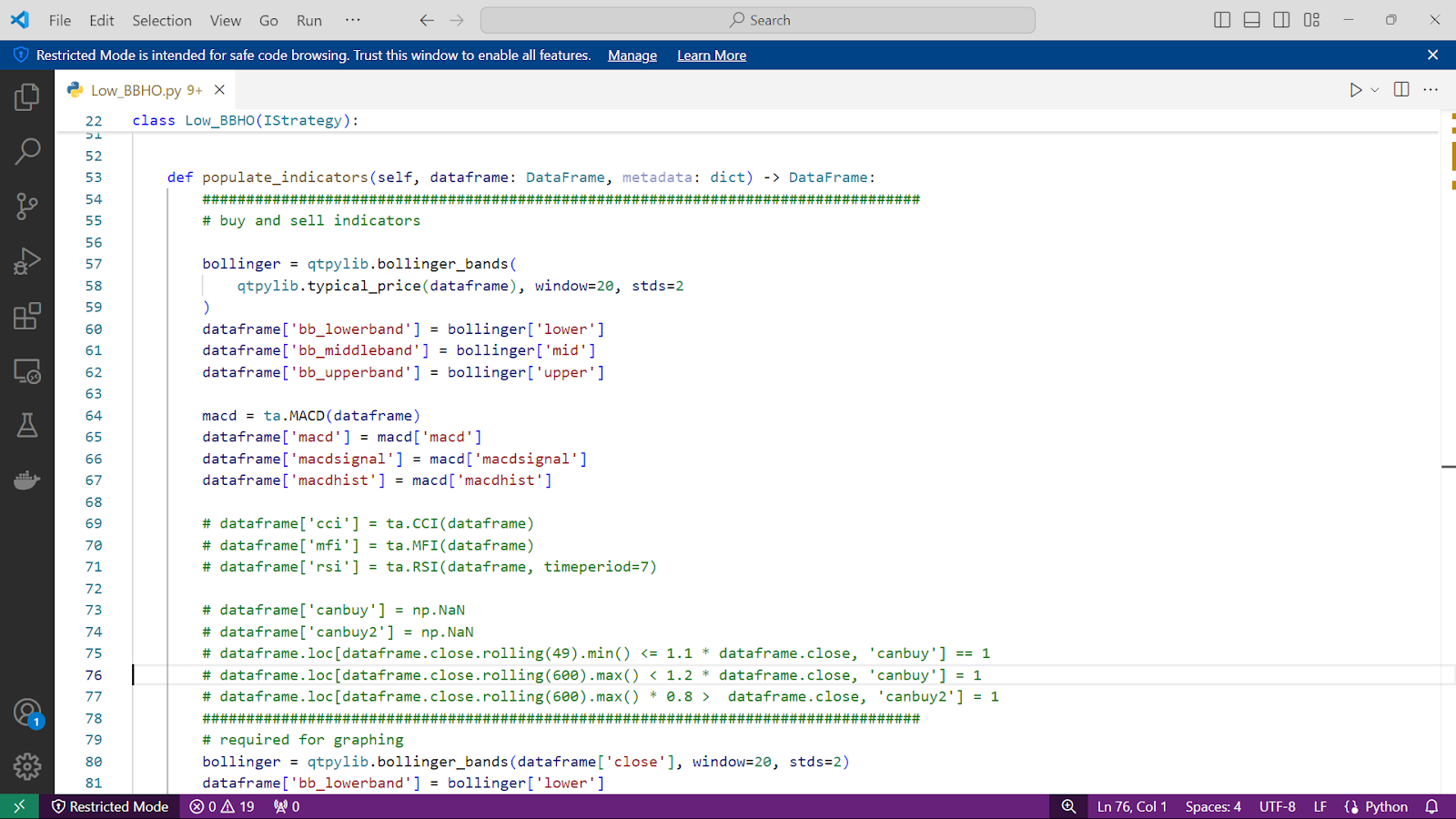

The indicators central to the Low_BBHO strategy revolve primarily around Bollinger Bands and the MACD. Additional indicators such as CCI, MFI, and RSI are commented out, perhaps for further exploration or refinement.

Bollinger Bands, calculated here with a standard 20-period window and 2-standard deviation bands, provide a range for assessing price volatility and spotting extremes. The lower band, is used with the entry signal, with the strategy buying when the closing price dips to 98% of this lower boundary.

The MACD indicator is used in the dataframe too but not directly tied to buy or sell conditions, so eventually useless, and will not be explained further anymore.

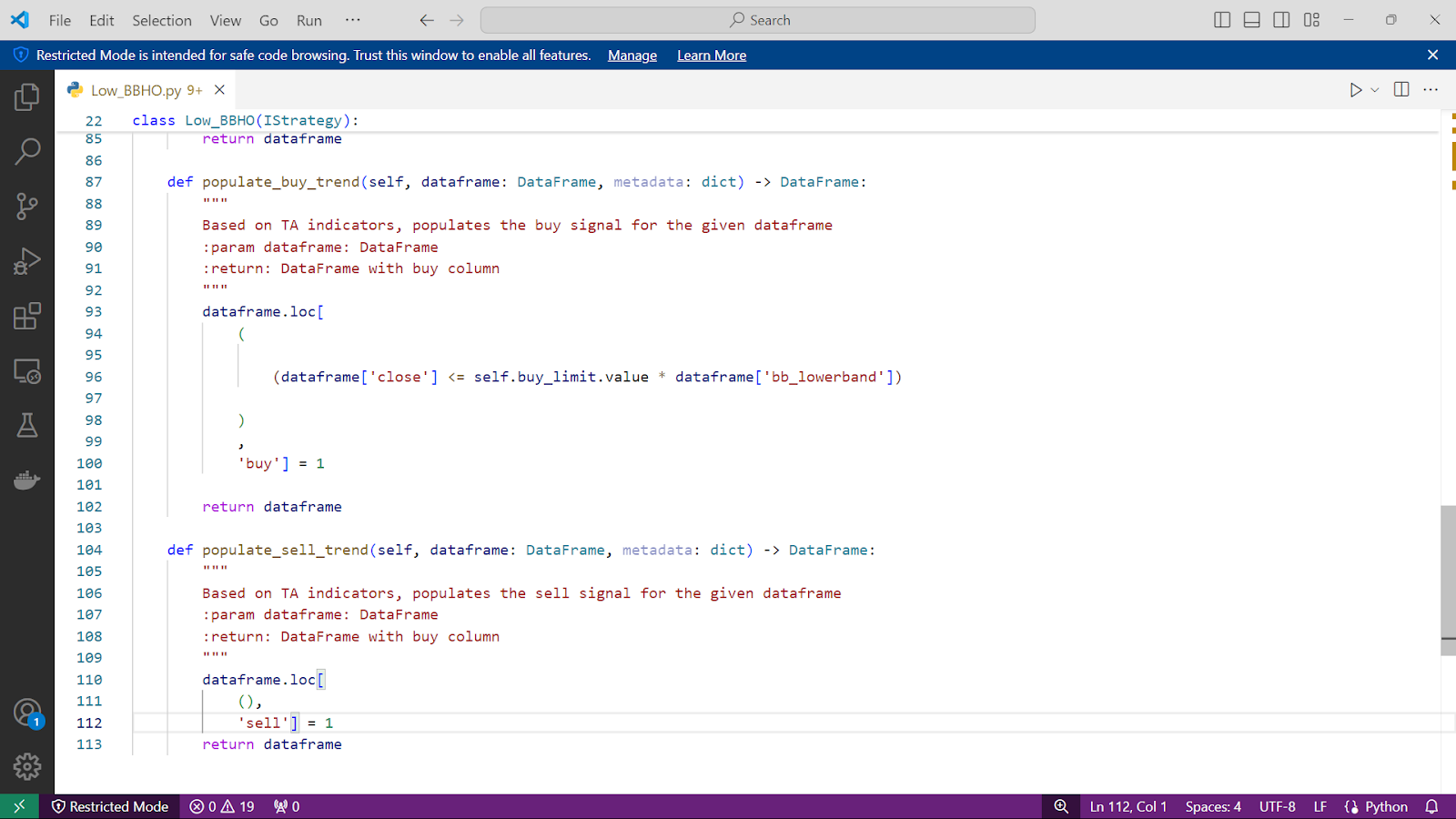

The entry logic, encapsulated in populate_buy_trend, is straightforward and based purely on Bollinger Bands. It signals a buy when the price is equal to or less than 98% of the lower Bollinger Band value. This conservative buy limit allows the strategy to take advantage of downward price movements, potentially catching a price rebound near its perceived lower extreme.

The exit conditions in populate_sell_trend, on the other hand, is completely empty. This suggests that, by default, the strategy relies only on Freqtrade’s built-in ROI and stop-loss configurations for exits. The lack of indicator-based exit signals could be a double-edged sword: it can simplifying the strategy. But it can also limit the flexibility to respond dynamically to trend reversals or overbought conditions.

Overall the strategy is simple to understand and explain. Let’s find out if this simplicity can be used to it’s advantage and create a good gain in the market.

Backtest results

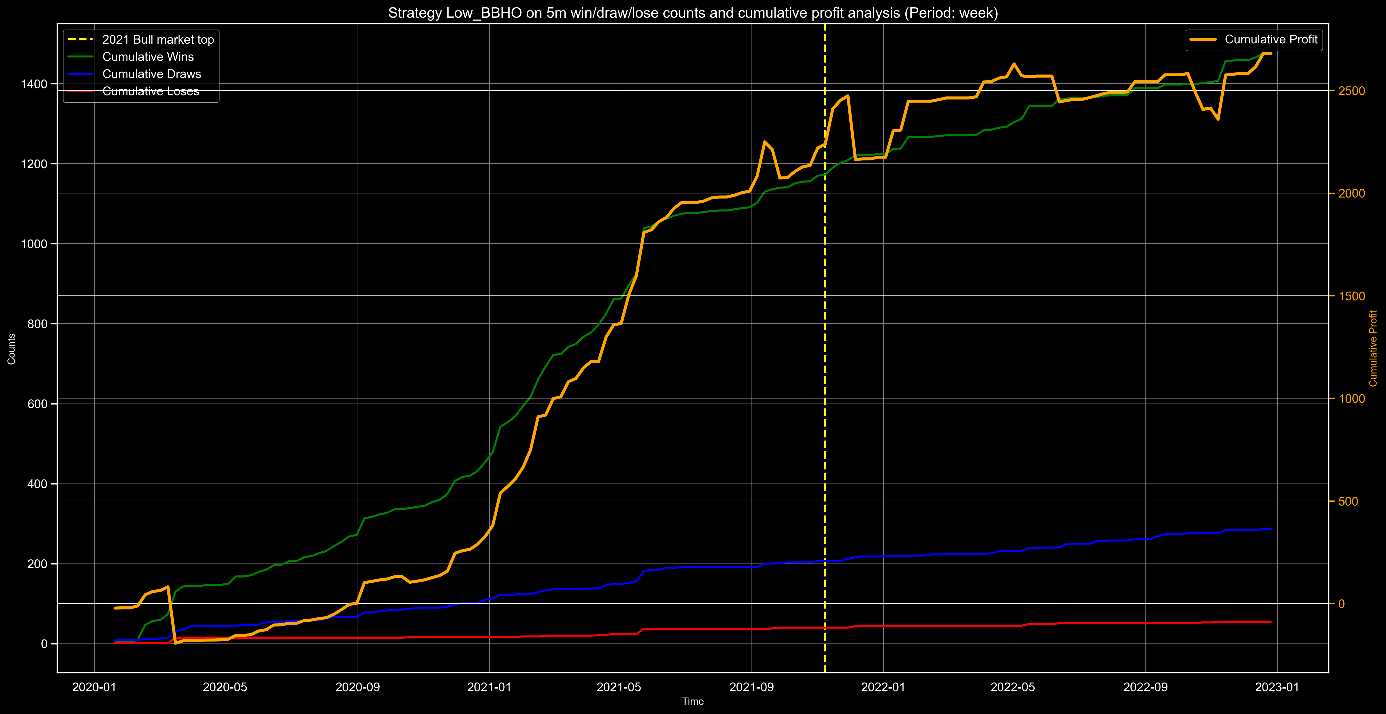

The Low_BBHO strategy shows steady cumulative profits with minimal losses, excelling in high-frequency trading on the 5 minute timeframe. Wins consistently rise, especially during the 2020-2021 bull market, and continue post-peak, highlighting the strategy's resilience across conditions. Minimal losses and draws reflect effective entry filters, seemingly making it a good choice for capturing consistent gains, even as markets shift.

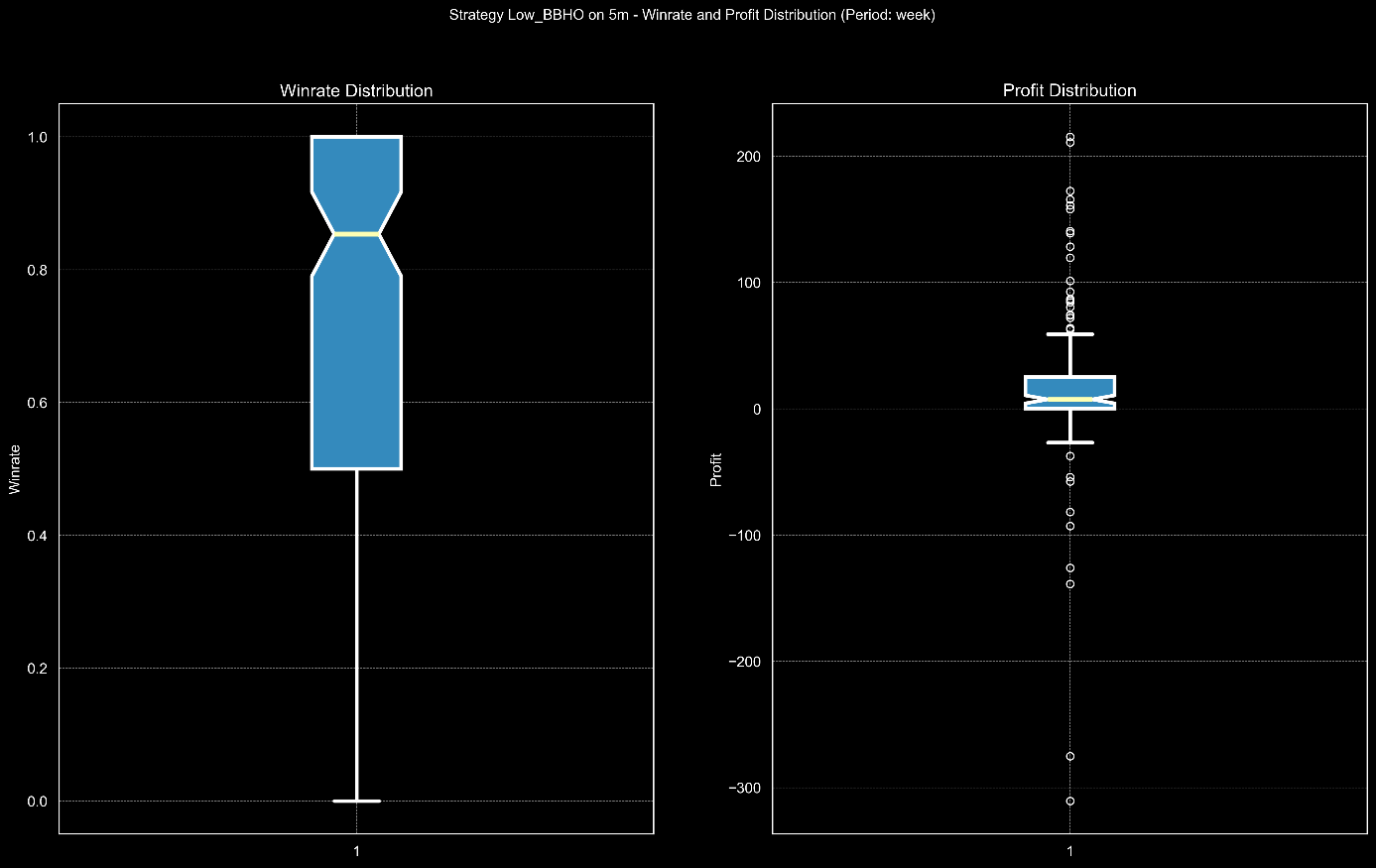

The "Winrate Distribution" plot shows a relatively wide range of win rates, with a median close to 0.9, indicating that the strategy generally wins around 90% of the time. This high win rate is promising, although the distribution's spread suggests that performance can vary significantly under different market conditions.

The "Profit Distribution" plot, however, reveals a more complex picture. The median profit is slightly positive, there is a notable spread, with a mix of high outliers and some deep losses. This spread indicates that while the strategy has the potential for occasional significant gains, it also encounters periods of substantial losses, which can impact overall profitability.

So it looks like the strategy boasts a strong win rate, but profit outcomes are mixed. The potential for high outliers is promising, but risk management may need to address the frequent smaller losses seen in the distribution.

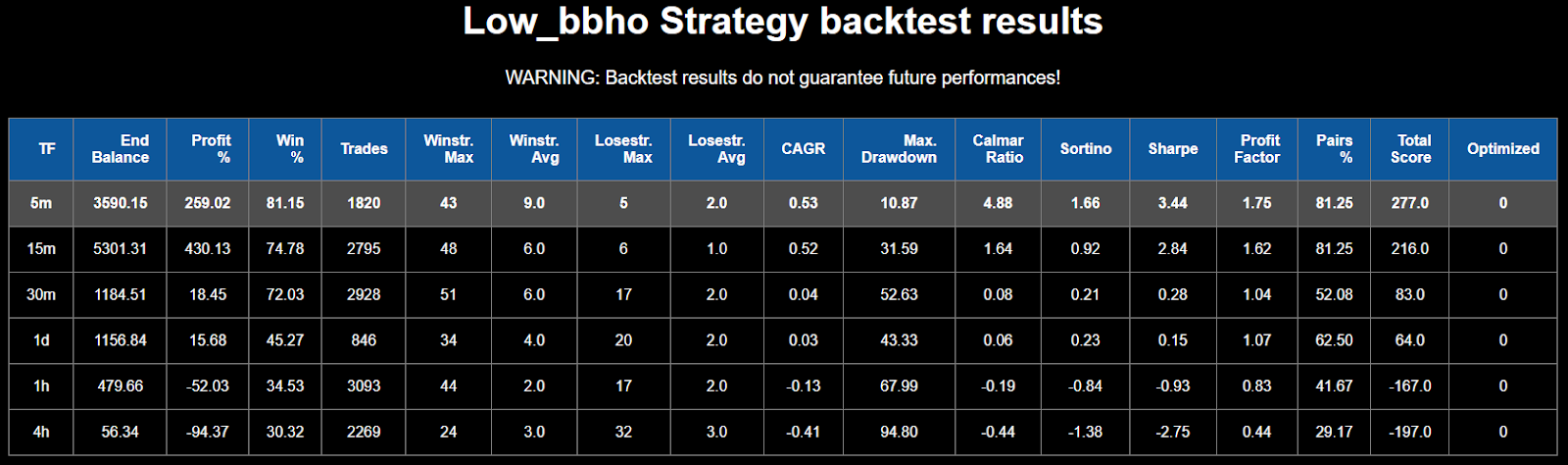

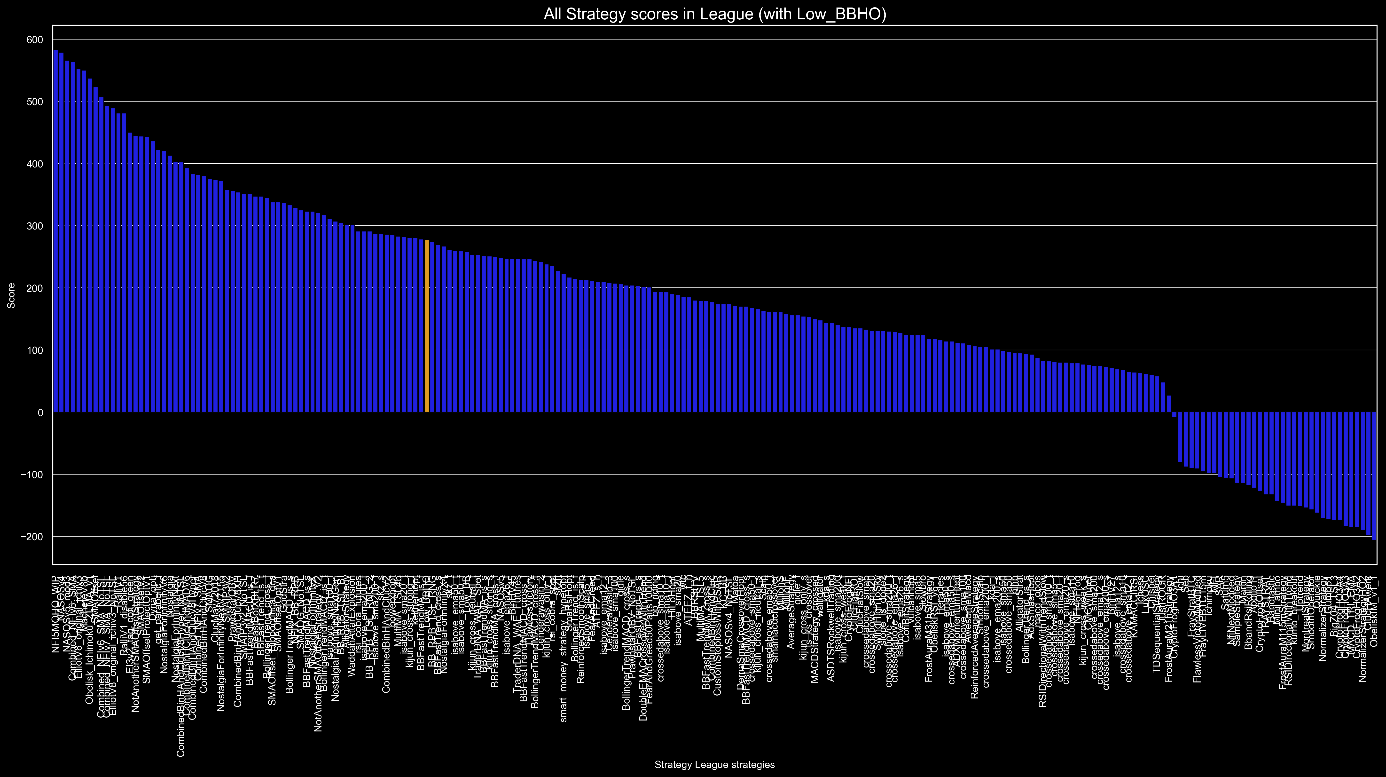

I found out that I could run this algorithm on all the timeframes I usually test. You can clearly see that this algo is designed to be used on the smaller timeframes since the 5, 15 and 30 minutes have the highest scores.

On the 5-minute timeframe, the strategy shows a strong performance with a total profit of 259%, a high win rate of 81.15%, and a Sharpe ratio of 3.44, indicating good risk-adjusted returns. The maximum drawdown is manageable at 10.87%, and the profit factor of 1.75 suggests the strategy earns $1.75 for every $1 lost, making it a solid choice for high-frequency trading. The high win streak (43) and low loss streak (5) add to the reliability of this timeframe.

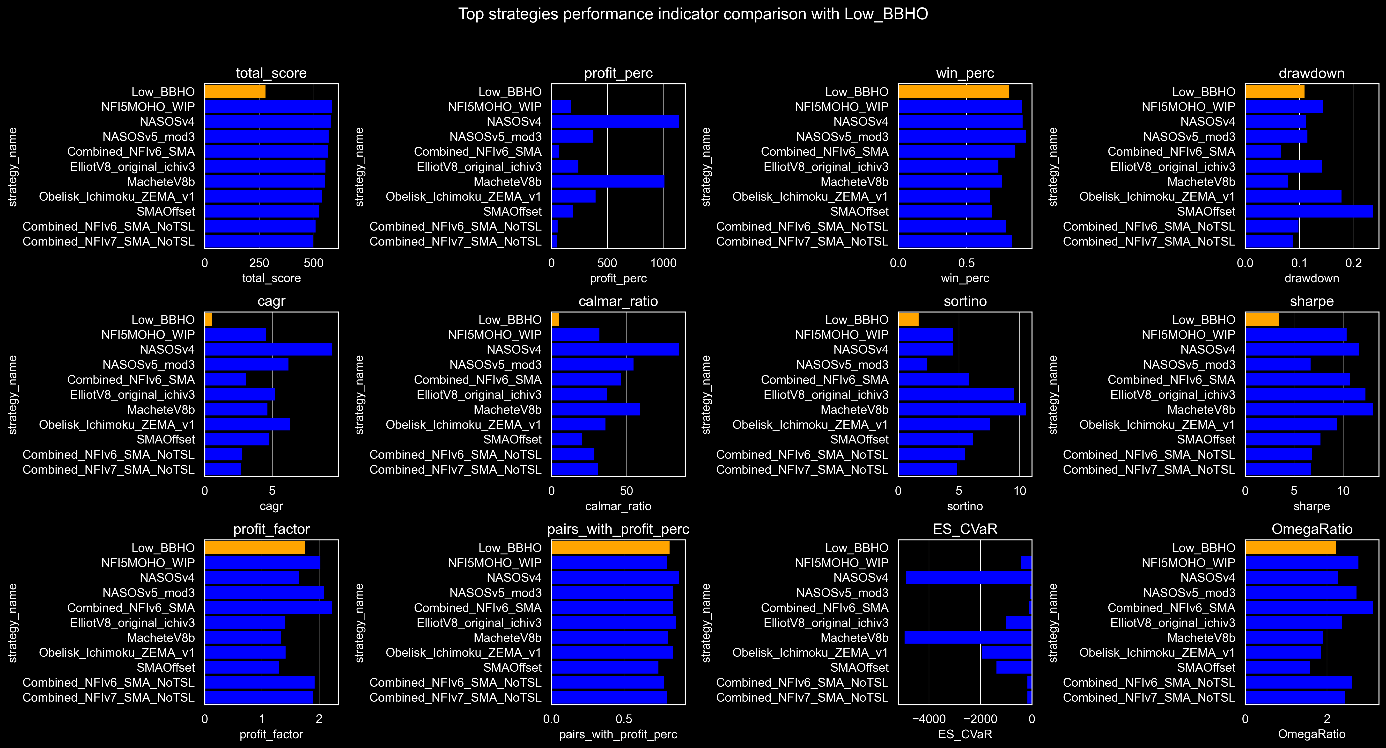

This performance comparison chart provides a detailed breakdown of how the Low_BBHO strategy stacks up against other leading strategies across multiple key indicators. Some noticeable mentions from this plot are:

The win percentage, which is notably high and a strong indicator of consistency.

Its low drawdown is another positive attribute. It is not the lowest, but certainly also not the highest. So it minimizes losses effectively.

The profit factor outshines some other, better performing algorithms.

And the way most coins respond to successful trading this algorithm is also worth mentioning.

So all in all, this Low_BBHO algorithm is a stable and consistent trading strategy, and excels in maintaining a high win rate and low drawdown. And this in relation to the really simple strategy rules it has. It looks to be a strategy that is ideal for steady gains in high-frequency trading. However, it leads in overall reliability, it is more conservative in terms of profit maximization and risk-adjusted returns compared to other top-performing strategies.

Before you think about using this algorithm in real life, please remember that you first have to do an extensive backtest AND forward test on your own personal environment because my results do not necessarily mean that this strategy will perform well in your situation as well.

And with these findings I am at the end of this post. I hope you got some useful information from this and if you are going to use this algorithm, maybe you want to add your feedback to this post so that other Patrons can benefit from your information too.

Thank you very much for reading and being a Patron.

And I will see you in the next post.

Goodbye!